Austin Real Estate Market Update – June 11, 2025

Austin Housing Market Update – June 11, 2025: Listings Near Record, Buyer Power Grows

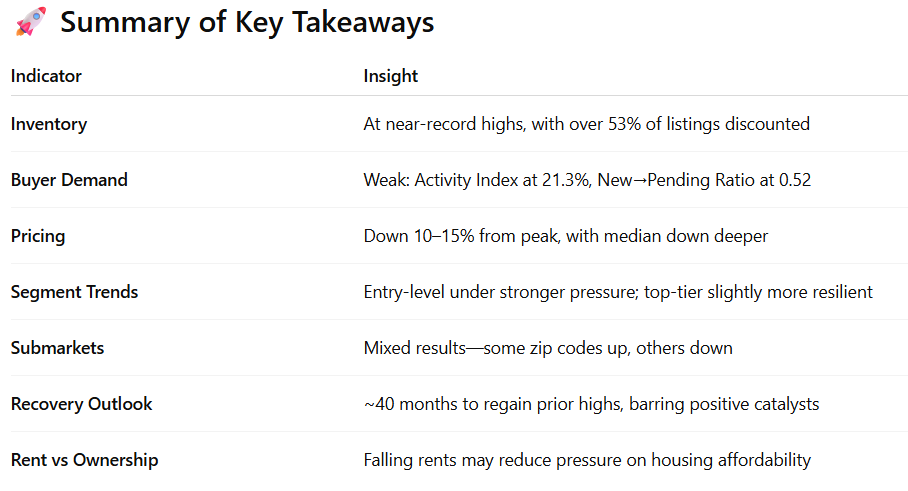

Market Context: Inventory Peaks and Price Sensitivity : As of June 11, 2025, the Austin metro area is experiencing historically high active residential inventory, with 17,426 active listings, just 115 units below the all-time high of 17,541 recorded two days prior on June 9. This surpasses the 2024 peak of 15,503 listings (July 15, 2024), indicating a substantial increase in unsold inventory year-over-year. Of these active listings, 54.1% have undergone price drops, which reflects significant pricing resistance in the market. This figure is not only indicative of overpricing or seller expectations lagging market reality, but also highlights the sheer volume of sellers competing for a dwindling pool of buyers.

Demand Conditions: Shrinking Absorption and Buyer Hesitation : The Activity Index, a measure of market absorption, currently sits at 21.3%, which is a 14.1% decline from 24.8% in June 2024. An Activity Index below 30% strongly suggests a buyer’s market, further confirmed by the Market Health Index (MHI) of 20.0% and Inventory Stress Index (ISI) of 6.9%—both well within thresholds that favor buyers. The Months of Inventory (MOI) has climbed to 6.19, up from 5.14 in June 2024, marking a 20.4% year-over-year increase. According to your internal classification system (Buyer’s Market = 7.0+ MOI), Austin is teetering on the edge of a full buyer's market. Inventory at this level means listings are sitting longer, and sellers are more likely to concede on price, incentives, or repairs to get contracts executed.

Supply Surge: New Listings Outpacing Buyer Demand : Year-to-date, the market has seen 26,560 cumulative new listings, which is 18.5% above the 25-year historical average, but still 3.7% below 2024 levels, indicating sellers are returning to the market, albeit slightly more cautiously than last year. However, cumulative pending sales from January to June total only 20,208, which is 16.6% lower year-over-year and 7.2% below the historical average. This divergence between supply and absorption has created a sharp imbalance, reflected in a cumulative gap of 6,352 listings—the largest disparity since 2004, when the market saw a similar glut.

New Listing to Pending Ratio: Systemic Imbalance Confirmed : The monthly New Listing to Pending Ratio now stands at 0.55, and the year-to-date average is 0.66. For historical context, the 25-year average is 0.81, indicating that the pace of absorption has slowed considerably. This ratio is crucial because it visualizes market fluidity. In a balanced market, the number of new listings should roughly match the number of homes going under contract. At 0.66, we're seeing 34% fewer homes going under contract for every new listing than we’d expect in a healthy market.

Sales Velocity and Sales Density: Further Signs of Contraction : In June 2025, 2,712 homes sold, and year-to-date sales are 14,805, which is 7.3% below the same period in 2024 but still 7.2% above the 25-year average. While this appears modestly positive, adjusted metrics like sales per 100,000 population (581, down 9.5% YoY and 20.8% below average) and sales per 1,000 Realtors (797, down 3.3% YoY and 24.9% below average) show that the broader market efficiency is deteriorating. The takeaway here is that despite a relatively decent absolute volume of sales, the productivity of the market relative to its population base and agent workforce has dropped, echoing trends seen during prior downturns.

Pricing: Peak-to-Trough Declines and Long-Term Recovery Outlook

Average Sold Price: Currently at $604,742, down $77,197 (-11.3%) from the May 2022 peak of $681,939.

Median Sold Price: Now $466,125, down $83,875 (-15.25%) from the $550,000 peak in May 2022.

These declines represent meaningful retractions in asset values and align with market corrections seen in past real estate cycles. The -12.87% drop in median prices versus 36 months prior confirms the prolonged nature of this correction. If we assume the bottom has been reached, based on the 25-year compound appreciation rate of 5.129%, it would take 42 months (November 2028) for median prices to recover to their 2022 peak of $549,185. This implies an extended low-growth environment, absent of external stimuli like falling interest rates or demographic booms.

Segment Analysis: Price Sensitivity Across the Market

Even high-performing market segments have softened:

Top 25th percentile prices: Down 2.3%, and price per square foot down 3.3%

Bottom 25th percentile prices: Down 2.8%, and price per square foot down 3.7%

This suggests that the market correction is not just impacting the entry-level or investor segments but is broadly distributed. However, marginally greater compression at the lower quartile may point to tighter affordability constraints and higher sensitivity to mortgage rates in that cohort.

City-by-City Performance: Diverging Recovery Paths : Only 11 cities reported year-over-year increases in median sold prices, while 18 cities saw declines, and 1 city remained flat. This is consistent with a fragmented market where micro-markets—driven by local schools, taxes, and new construction—are performing independently rather than rising with a market-wide tide. This may suggest that investors and buyers should shift away from blanket strategies and instead adopt hyper-localized analysis when evaluating acquisition or listing opportunities.

Trend Implications and Forward Outlook : The widening gap between new listings and pendings, coupled with increasing months of inventory and elevated price reductions, makes a compelling case for the market being deep in a correction phase. The absence of urgent buyer demand—despite price drops and improved relative affordability—indicates that the broader market is still digesting prior excesses. Unless mortgage rates decline significantly or job/income growth accelerates, it is unlikely that absorption will return to pre-2022 levels in the short term. Furthermore, with June 2025 new-to-pending ratios (0.55) below every historical June average since 2000, there is no empirical support for an immediate rebound.

Conclusion : In sum, the Austin real estate market as of mid-June 2025 is defined by historically high inventory, muted demand, slower absorption, and continued downward price pressure. This environment presents opportunities for buyers but signals caution for sellers and developers. Pricing strategy, property condition, and local submarket performance will be critical to navigating the remainder of 2025, as the broader market recalibrates after a historic run-up and correction cycle.

Scroll down to view the full Austin Daily Real Estate Briefing PDF for June 11, 2025, with today's data.

FAQ: What Buyers and Sellers Want to Know About the Austin Housing Market – June 2025

Is the Austin housing market crashing in 2025?

No, the Austin housing market is not crashing in the traditional sense of the word, but it is undergoing a significant multi-year correction. As of June 2025, home prices have fallen approximately 14.6% from their May 2022 peak, and active inventory has surged to near-record highs at 17,456 listings. This is not a sudden collapse caused by a financial crisis, but rather a prolonged adjustment following an overheated pandemic-era market. The drop in prices has been orderly, with many sellers reducing prices gradually, and most of the correction is being driven by a mismatch between supply and buyer demand. Despite the sharp slowdown in activity, the fundamentals of employment and migration trends in Austin remain relatively stable, which means the market is cooling, not collapsing.

Is it a good time to buy a home in Austin, Texas right now?

June 2025 is shaping up to be a favorable environment for buyers in Austin. With the Months of Inventory currently at 6.19, the market is leaning toward a buyer’s market, giving purchasers more leverage in negotiations. Over 53% of listings have seen price reductions, and sellers are more likely to offer concessions such as closing cost credits or rate buydowns. Although mortgage rates remain relatively high, price drops and increased inventory provide opportunities for well-qualified buyers to secure better deals, especially in markets with limited competition. Buyers who plan to stay in their home for several years and are comfortable with today’s financing terms—or who plan to refinance later—may benefit from locking in now while sellers are motivated.

How much have home prices dropped in Austin since the peak?

Home prices in Austin have declined considerably since their peak in May 2022. The median sold price has fallen from $550,000 to $470,000 as of June 2025, which represents a 14.55% decline. The average sold price is now $613,577, down about 10% from the peak of $681,939. This correction has taken place gradually over three years and reflects both declining buyer demand and rising inventory levels. While many cities have seen modest pullbacks, Austin’s decline is among the more pronounced in Texas due to its rapid appreciation during the 2020–2022 boom. If historical appreciation patterns return, it may take until late 2028 for prices to fully recover to peak levels, assuming a compound growth rate of 5.1%.

Why are there so many active listings in Austin right now?

The rise in active listings—currently at 17,456, just below the all-time high—is the result of several converging factors. First, many homeowners delayed listing in 2022 and 2023 due to market uncertainty, leading to a buildup of pent-up supply. Second, as interest rates remained elevated, buyer activity slowed significantly, leaving more homes on the market for longer periods. Third, a wave of new construction homes that began during the pandemic is now reaching completion, especially in suburban markets like Leander, Georgetown, and Kyle. Finally, some investors and institutional owners are exiting the market or restructuring portfolios, adding even more supply. The result is a high-inventory environment where buyers have more choices, and sellers face greater competition.

Will Austin home prices go back up soon?

While Austin home prices may eventually recover, it is unlikely that they will rise significantly in the short term. According to historical appreciation trends, Austin’s 25-year compound annual growth rate is 5.1%. If the market has indeed bottomed out with a median price of $470,000, and appreciation returns to its long-term norm, it would take approximately 40 months—until September 2028—to return to the 2022 peak of $550,000. However, short-term gains will be heavily dependent on mortgage rates, job growth, and consumer sentiment. Unless mortgage rates fall sharply or a major demand surge occurs, home values in Austin are expected to increase slowly and unevenly over the next few years.

Have a Question or Want to Dive Deeper?

If you’d like a custom breakdown of the data, want help interpreting today’s market trends, or just have a question about buying or selling in Austin, let us know. Fill out the form below and a member of our team will get back to you promptly.